Is my Investment Safe?

Mountain Investment invests primarily in second mortgages, which carry a higher risk of default but offer higher returns. However, Mountain Investment is able to minimize the risk of default through conservative appraisal values. We only work with carefully selected, licensed appraisers to get an accurate value of the underlying real estate. Mountain Investment also practices conservative lending to avoid excessive risk.

How is the business regulated?

Mountain Investment’s money-raising and other activities are regulated through the Alberta Securities Commission under National Instrument 31-103. This is a relatively new regulation that covers Alberta-based Mortgage Investment Corporations and Mortgage Syndicators that qualify. Mountain Investment is not registered to conduct any money-raising activities in any province or jurisdiction other than Alberta. However, we are extra-provincially registered and otherwise “licensed” to conduct our mortgage lending activities in B.C., Saskatchewan, Manitoba and Ontario.

How are distributions taxed?

Mountain Investment does not pay a corporate level of income tax, but fully distributes all earnings, which are taxed as interest income in the hands of each shareholder. Consult your tax professional for the implication to your overall tax liability.

How do I Invest?

Mountain Investment offers Non-Voting Class A shares sold at NAV (Net Asset Value)≈$100.00 each. When you purchase your shares in Mountain Investment (MI), we create a file for you and open a general ledger account in our accounting system to keep track of your investment and dividends for reporting to you and regulatory agencies as required.

Shares of MI are not listed on any security exchange and are unlikely to be at any time in the future. Lack of liquidity is therefore an issue for potential investors to be aware of. However, MI does redeem shares under certain conditions including cash availability and written notification from the shareholder.

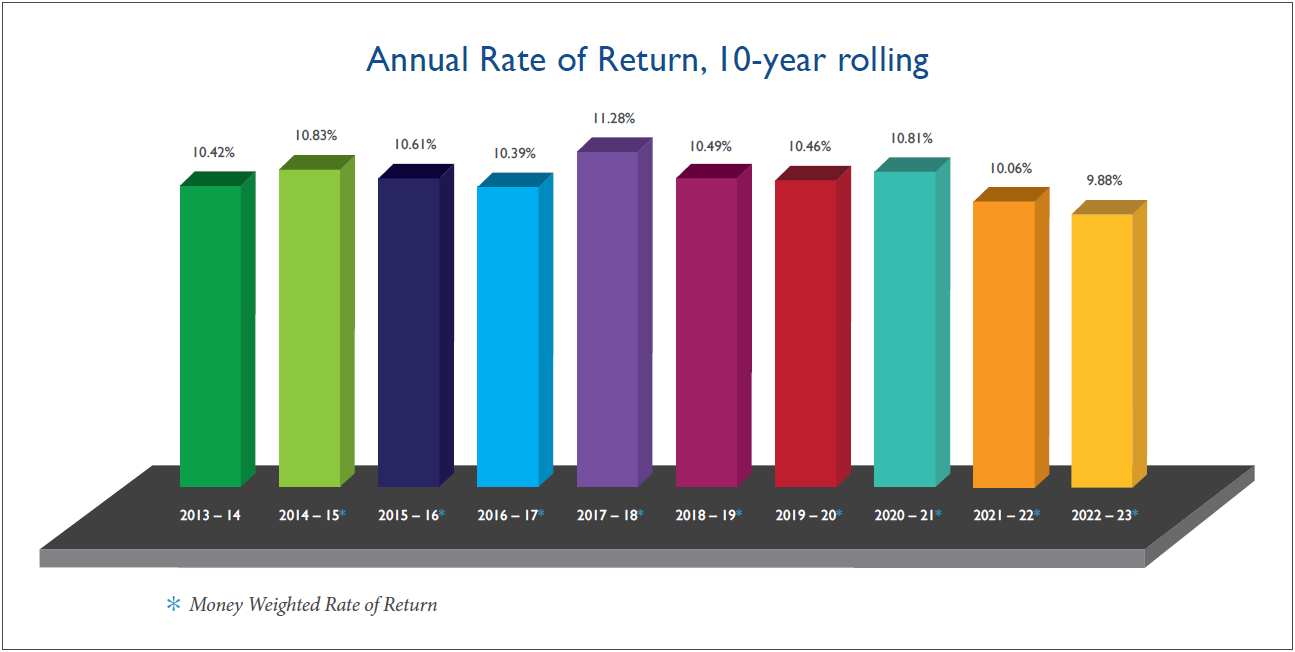

What kind of returns can I expect?

Obviously, management undertakes extensive internal planning and rates of return factor high in that process. Forecasting rates of return is not an exercise we feel is valid in this forum and the variables such as default rates, oversight costs and capital utilization are not controllable and have an impact on return. It is relevant to view our historical results as an indication of management performance, but in no way should historical returns be considered a forecast of future returns.

What are the risks in investing in second mortgages?

For many borrowers, a second mortgage is necessary to working out financial difficulties, and the higher interest rate and costs are justified in order to obtain mortgage financing. Some borrowers are not able to resolve their financial difficulties and will default on their mortgage or opt to sell their home in the real estate market. As a result, default rates are typically higher with second mortgages than with mortgages insured through chartered banks. Our conservative underwriting, lending policy and professional appraisal values are the basis for ensuring full realization of all monies due in the event of default. Even so, for various reasons, losses do occur.

There are other risks associated with real estate mortgage investment and in Mortgage Investment Companies and those risks are discussed in more detail in the Disclosure section.

Why do people borrow high rate money?

Prime market lenders focus heavily on personal circumstances of the borrower, such as credit score and employment, while placing little emphasis on the value of a borrower’s assets. As a result, people with a credit challenge may be unable to borrow from prime market lenders, even when they have significant assets. Private market lenders allow individuals with high asset value to access financial resources through mortgage borrowing.

Furthermore, Canadian employment is increasingly shifting away from long-term employment by large entities to self-employment and contract work. This results in uncertain or unverifiable income that causes many people to lose access to the prime credit market, even when they possess a clean credit history. These people rely on private lenders such as Mountain Investment to borrow money, even if it is at a higher rate.

What’s the future for Mountain Investment?

Rather than aggressively raising new capital, Mountain Investment will strive for steady organic growth. This will moderate risk by reducing the pressure to place ever more mortgages. To increase efficiency, Mountain Investment will continuously look at ways to improve accounting, administrative procedures and technology. Investors will benefit from better reporting, faster period closes and increased checks and balances.

Mountain Investment will work towards diversifying our network of mortgage brokers and establishing long-term relationships with brokers to better meet the needs of the company.